Government of British Columbia Government Organization ● 51,779 Likes

Starting in January 2017, BC is partnering with first-time homebuyers. With the new BC HOME Partnership program, you could be eligible for a down payment loan of up to 5% of the purchase price of a home. #BCFirst http://ow.ly/lSmN307cBRr

If you’re entering the market to buy your first home, the B.C. government is launching a new program to partner with you on the down payment for your mortgage, Premier Christy Clark announced today.

“We believe every British Columbian deserves a place to call home,” said Premier Christy Clark. “We’ve invested in affordable rental housing, we’ve invested in transitional and emergency housing, and now we’re partnering with first-time buyers to make the purchase of their first home more affordable.”

Saving for a mortgage down payment can be hard for first-time homebuyers. The B.C. Home Owner Mortgage and Equity Partnership program contributes to the amount first-time homebuyers have already saved for their down payment, providing up to $37,500, or up to 5% of the purchase price, with a 25-year loan that is interest-free and payment-free for the first five years. Through the B.C. HOME Partnership program, the Province is investing about $703 million over the next three years to help an estimated 42,000 B.C. households enter the market for the first time.

“The first step into the market can be the hardest step, so our government will partner with homebuyers to help them achieve their minimum down payment,” said Rich Coleman, Minister of Natural Gas Development and Minister Responsible for Housing. “This partnership can help lower their monthly costs in the first five years, and help make home ownership more affordable. This partnership program is another important way we’re taking action on housing affordability.”

During the first five years, no monthly interest or principal payments are required as long as the home remains the homebuyer’s principal residence. After the first five years, homebuyers begin making monthly payments at current interest rates. Homebuyers will repay the loan over the remaining 20 years, but may make extra payments or repay it in full at any time without penalty. The loan must be repaid in full when the home is sold or transfered to another owner.

[embed]https://youtu.be/1nA2RooGEyg[/embed]

To be eligible, buyers must be preapproved for an insured high-ratio first mortgage (mortgage down payment is less than 20% of the home price). On completion of the sale, program funds will be advanced and the loan will be registered as a second mortgage on the property’s title.

Other programs are available to help first-time buyers save on property transfer tax. The First Time Home Buyers Program can save first-time buyers up to $7,500 when purchasing a home valued up to $475,000. Or, first-time buyers can access the Newly Built Homes Exemption, which can save buyers up to $13,000 in property transfer tax when purchasing a newly constructed or subdivided home worth up to $750,000.

The B.C. Home Owner Mortgage and Equity Partnership program will start accepting applications Jan. 16, 2017.

Key Facts:

The Province’s commitment to housing action is driven by six key principles:

- Ensuring the dream of home ownership remains within the reach of the middle class

- Increasing housing supply

- Smart transit expansion

- Supporting first-time home buyers

- Ensuring Consumer Protection

- Increasing rental supply

- The B.C. government has committed $855 million over five years, including $575 million this year, to support the construction or renovation of 4,900 units of affordable housing throughout the province.

- Since 2001, the B.C. government has invested $4.9 billion to provide affordable housing for low income individuals, seniors and families.

- More than 104,000 B.C. households benefit from a diverse range of provincial housing programs and services.

Learn More:

Learn how to apply: https://news.gov.bc.ca/files/Housing_Campaign_HOME.pdf

To learn more about the Province's actions on housing affordability, visit: http://housingaction.gov.bc.ca/

For additional details about the B.C. Home Owner Mortgage and Equity Partnership program, please visit: https://homeownerservices.bchousing.org/

B.C. Home Owner Mortgage and Equity Partnership program, BC Housing:

Phone: 604 439-4727

Toll Free Number: 1 844 365-4727

Backgrounders

B.C. Home Owner Mortgage and Equity Partnership program details

Am I eligible for a partnership loan?

The program supports eligible first-time homebuyers who are approved for an insured high-ratio first mortgage. To qualify for the program, all individuals on title must:

- Have been a Canadian citizen or permanent resident for at least five years.

- Have resided in British Columbia for at least one year immediately preceeding the date of application.

- Be a first-time buyer who has not owned an interest in a residence anywhere in the world at any time.

- Use the property as their principal residence for the first five years.

- Purchase a home that has a purchase price price of $750,000 or less (excluding taxes and fees).

- Obtain a high-ratio insured first mortgage on the property for at least 80% of the purchase price.

- Have a combined, gross household income of all individuals on title not exceeding $150,000.

- Have saved a down payment amount at least equal to the loan amount for which the buyer applied.

What do I do and how do I apply?

Step 1: Get preapproval for an insured first mortgage from your financial lending institution.

Step 2: Apply to BC Housing for the B.C. Home Owner Mortgage and Equity Partnership program loan. If you are eligible, you will receive confirmation of eligibility and Homebuyer’s Kit, which includes information for your lender, real estate licensee, and lawyer/notary public.

Step 3: Find your home and provide the details of your planned purchase to BC Housing for approval.

Applications for the program will be accepted starting Jan. 16, 2017, for purchases that will close on or after Feb. 15, 2017.

What information will I need to apply?

Buyers can begin gathering the documents they’ll need to submit an online application. Buyers will need:

- Proof of status in Canada and residency in British Columbia.

- Secondary identification (must include your photo).

- Proof of income and tax filings.

- Insured first mortgage pre-approval.

More information about these requirements: https://homeownerservices.bchousing.org/

Support for first-time buyers using the B.C. Home Owner Mortgage and Equity Partnership program

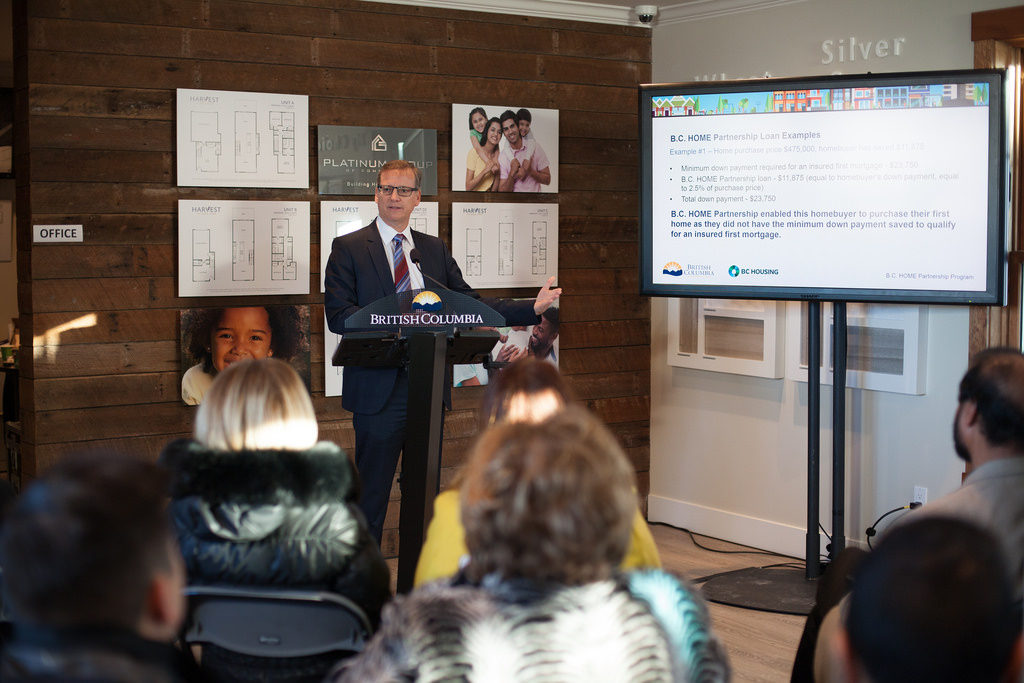

Example #1: Home purchase price – $475,000

This first-time buyer has saved $11,875 towards their down payment, or 2.5% of the home’s purchase price. Through the progam, the Province will contribute $11,875, equal to the buyer’s 2.5% down payment. This brings the total down payment to $23,750 or 5% of the home’s purchase price, as required by Canada Mortgage and Housing Corporation. This loan is interest and payment-free for the first five years.

As a first-time buyer, this person can also qualify for the First Time Home Buyer’s exemption for the Property Transfer Tax, saving: $7,500.

The B.C. HOME Partnership program enabled this buyer to purchase their first home as this buyer did not have the minimum down payment saved to qualify for an insured first mortgage.

Example #2: Home purchase price – $600,000 This first-time buyer has saved 5% of the home’s purchase price towards their down payment, or $30,000. Canada Mortgage and Housing Corporation requires a 5% down payment for the first $500,000, and 10% for the remaining portion. This means the minimum down payment required for a home valued at $600,000 is $35,000. This loan is interest and payment-free for the first five years.

If this is a newly built home, the buyer can also qualify for the Newly Built Home Exemption for the Property Transfer Tax, saving: $10,000.

The B.C. HOME Partnership program will meet this buyer’s contribution of $30,000, bringing their total down payment to $60,000, and enabling this buyer to purchase their first home as they had not yet saved the minimum down payment required to qualify for a insured first mortgage.

Example #3: Home purchase price – $750,000

The first-time buyer in this example has saved 7% of the home’s purchase price as a down payment, or $52,500.

Canada Mortgage and Housing Corporation requires a 5% down payment for the first $500,000, and 10% for the remaining portion. This means the minimum down payment required for a home valued at $750,000 is $50,000.

The Province will meet the buyer’s contribution up to 5% of the home’s purchase price. In this example, the program will contribute $37,500 towards the down payment, allowing this buyer to put a total of $90,000 towards the down payment of their first home.

Assuming a 3% interest rate, this buyer will save $5,201 in interest payments during the first five years of their mortgage compared to if the buyer had purchased the home without the program.

In addition, if this is a newly built home, the buyer can also qualify for the Newly Built Home Exemption for the Property Transfer Tax, saving: $13,000.

anada Mortgage Professionals Association has done a great job of summarizing the rules changes. The four points below are the key take-a-ways, which outlines the definitive changes on the immediate horizon, but there is also consultation happening specific to "sharing of risk" in terms of mortgage defaults. The government would like to consider a shift from our current model of 100 per cent government-back mortgages to having lenders share some of the responsibility for default risk.

anada Mortgage Professionals Association has done a great job of summarizing the rules changes. The four points below are the key take-a-ways, which outlines the definitive changes on the immediate horizon, but there is also consultation happening specific to "sharing of risk" in terms of mortgage defaults. The government would like to consider a shift from our current model of 100 per cent government-back mortgages to having lenders share some of the responsibility for default risk.

![[dropshadowbox]](http://strongfitmortgage.com/wp-content/uploads/2015/08/Simmy-Sandhu-Banner650.jpg){kind=link}